When it comes to building an emergency fund, most people think of Fixed Deposits (FDs) or Debt Mutual Funds. But for investors in higher tax brackets, there’s another smart option—Arbitrage Funds. The real question is: Arbitrage Fund vs Debt Fund — which one should you choose for your emergency money?

Understanding Emergency Funds

An emergency fund is a safety net that you should be able to access quickly, without hassle. By definition, you shouldn’t spend more than an hour to get this money. Two key features define an effective emergency fund:

- Ease of Access – The money should be available almost instantly.

- Reasonable Returns – While safety is the priority, the funds should still earn some interest.

In terms of speed, Debit Cards are the fastest, followed by Fixed Deposits (FDs). Debt-based mutual funds can also be efficient, but some are still in the T+1 category, meaning you may need to wait a day or two for withdrawals.

This “time gap” can be easily solved when combined with a Credit Card—you can spend instantly and settle the dues once your redemption is credited. Therefore, it makes sense to classify emergency funds into two buckets:

- Fast Access – FDs, Debit-linked accounts, Wallets.

- Relatively Slower (T+1) – Debt Mutual Funds, Arbitrage Funds.

Once this classification is clear, parking emergency reserves in debt mutual funds becomes an easy and rational choice.

The Problem with Debt-Based Instruments

Debt funds and FDs have one drawback – Taxation. No matter how long you hold them, the gains are taxed at your income tax slab rate.

- If you are in the 30% slab, your post-tax returns shrink considerably.

- For those in the 10% or 20% slab, this may not hurt much.

This is where Arbitrage Funds enter the picture as a smarter substitute.

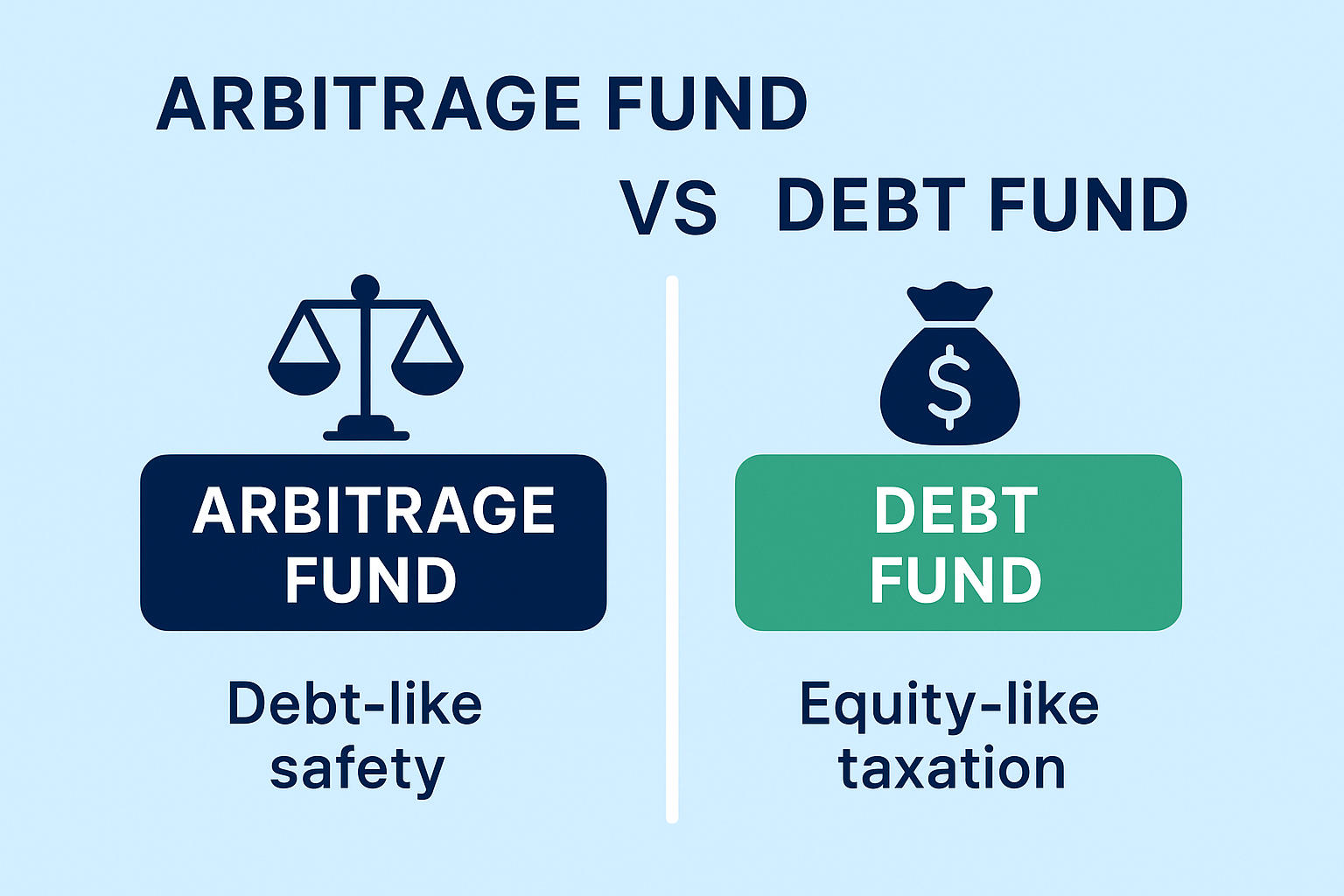

Arbitrage Funds – Equity Tax, Debt-like Safety

Arbitrage Funds are classified as equity funds for taxation purposes because they invest primarily in equity instruments.

- If redeemed within 1 year → Short-Term Capital Gains (STCG) tax of 20% applies.

- If held for more than 1 year → Long-Term Capital Gains (LTCG) tax of 12.5% applies.

This makes Arbitrage Fund particularly attractive for investors in the 30%+ tax bracket, as their tax outgo reduces drastically compared to debt funds.

How Do Arbitrage Funds Work?

The core idea comes from the age-old practice of arbitrage—profiting from price differences in two markets.

📌 Example: Buy diesel in Goa where it is cheaper and sell it in Maharashtra at a higher price to pocket the tax difference.

In financial markets, the concept is applied to equities and futures:

- Spot Market → Buy the stock at today’s price.

- Futures Market → Sell the same stock in the futures contract at a slightly higher price.

Since futures usually trade at a premium to spot price (due to interest rates, dividends, and market expectations), the fund locks in a risk-free spread.

This strategy:

- Eliminates market risk (since the buy and sell are simultaneous).

- Provides stable returns (usually between 5%–6.5% annually).

- Enjoys equity taxation benefits.

Why Arbitrage Fund Is Safe

Arbitrage Funds are often misunderstood as risky because they deal in equities. However, unlike typical equity funds, they do not speculate on market movements.

They buy and sell simultaneously, capturing the price difference without exposure to volatility. This makes them:

- Low-risk like debt funds

- Tax-efficient like equity funds

When Should You Use Arbitrage Fund for Emergency Money?

Arbitrage funds are ideal if:

- You are in the 30%+ tax bracket

- You don’t need instant liquidity (T+1 settlement works for you)

- You want better post-tax returns than short-term debt funds or FDs

For investors in lower tax brackets, short-term debt funds or FDs may still make more sense.

| Feature | Fixed Deposit (FD) | Debt Mutual Fund | Arbitrage Fund |

|---|---|---|---|

| Liquidity / Access | Instant (via Debit Card or premature withdrawal) | T+1 (sometimes faster with instant redemption options) | T+1 redemption |

| Returns | 5%–7% (fixed, depends on bank & tenure) | 4%–6.5% (market-linked, may fluctuate) | 5%–6.5% (linked to arbitrage opportunities) |

| Risk | Very low (bank guarantee up to ₹5 lakh under DICGC) | Low (but subject to credit risk, interest rate risk) | Very low (no market risk, only spread risk) |

| Taxation | Taxed as per slab (no indexation) | Taxed as per slab (no indexation) | Equity Taxation → <1 yr: 20% STCG, >1 yr: 12.5% LTCG |

| Best For | Very short-term parking, instant emergency use | Emergency fund (if okay with T+1) | Higher tax bracket investors seeking safe, tax-efficient returns |

| Drawback | Fully taxable as per slab | Tax-inefficient for 30%+ slab | Not instant (T+1), lower return in falling interest rate cycles |

Final Thoughts on Arbitrage Fund

For investors in higher tax brackets, Arbitrage Funds are an excellent substitute for debt funds—combining safety, stability, and tax efficiency. When used smartly as part of your emergency fund strategy, they can significantly improve your post-tax returns without compromising on safety.